UK Kidswear Market Report

The UK kidswear market is shifting from pure practicality toward greater expressiveness and inclusivity. This report analyzes leading brands from value-tier supermarket staples to fashion-forward players, examining how they differentiate through pricing, materials, and design. Key trends emerging include gender-neutral dressing with seasonless palettes, athleisure and oversized silhouettes mirroring adult fashion, and personality-driven graphics reflecting children's niche interests — pointing toward a future that balances durable basics with joyful self-expression.

Alice Clarke

"A data-led look at where UK kidswear is heading — and how brands can stay ahead"

The UK kidswear market has long been defined by value, comfort, and long-lasting basics, and whilst these attributes still remain a priority, there is a growing demand for more unique, bright, and trending pieces. Gender-neutrality is rising, supporting longer garment lifecycles and more inclusive hand-me-downs. At the same time, kidswear styles are mirroring adult trends, with athleisure and comfortwear dominating in both bright and muted colour palettes.

In this report, we analyse some of the leading UK kidswear brands, evaluate their current offerings, and explore the future trends that will shape the market. Overall, these shifts signal that the kidswear market is moving towards more expression and inclusiveness to align with modern family life.

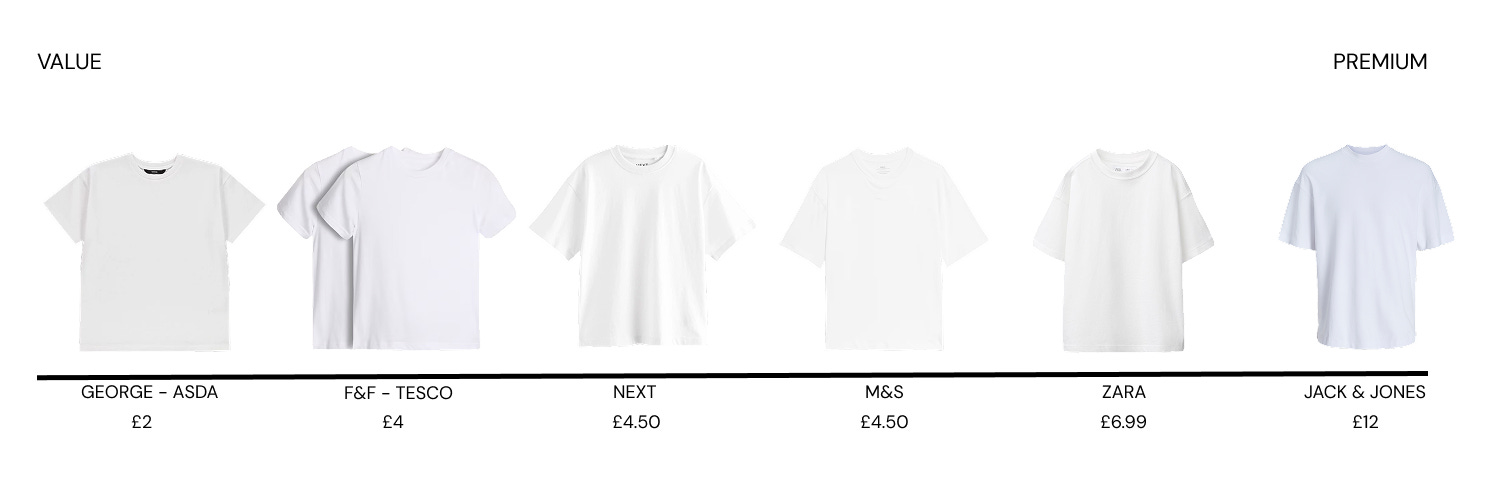

Price

When comparing similar items across brands, there is a clear price hierarchy, even when the core fabric remains the same. Supermarket staples F&F Clothing at Tesco and George at Asda sit at the most accessible end, with slim-fitted 100% cotton t-shirts for £2. Prices rise at the mid-tier, with Next and M&S both offering comparable tops for £4.50, differentiated through slightly more oversized silhouettes. Zara then follows at £6 with a similar oversized silhouette. At the premium end, Jack & Jones stands out at £12. While still within the cotton category, its use of 50% organic cotton and a more tailored silhouette justify the higher price through material quality and design distinction.

Material and Value

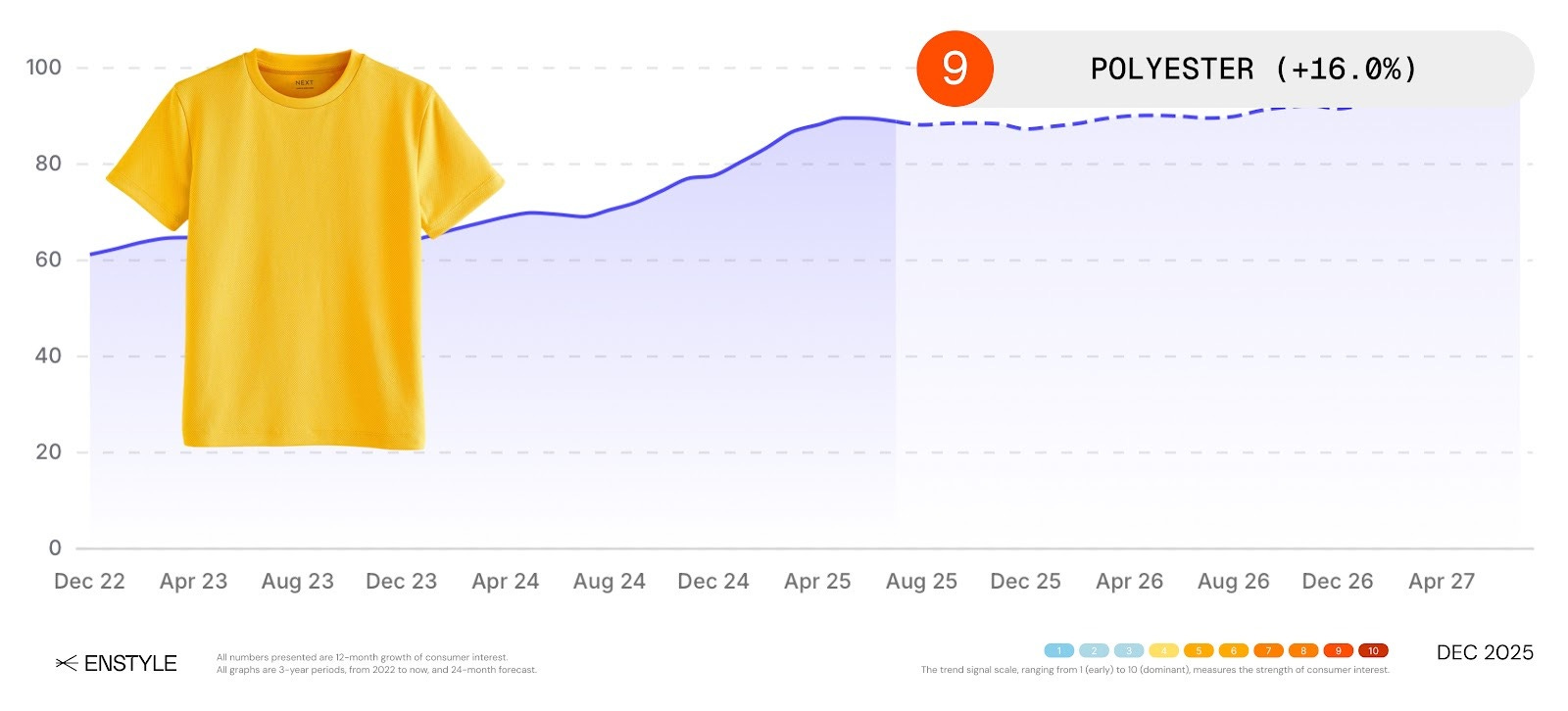

Looking further into fabric composition, supermarket staples like F&F at Tesco and George at Asda lead the value-driven space with an emphasis on practicality and affordability. Both brands utilise 100% cotton (+11.7%) as their leading fabric choice, followed by polyester (+16.0%), cotton-polyester blends (12.9%), aligning with their positioning of delivering key factors like price, convenience, and easy care. Functional design elements, including elastic waistbands, reinforced seams, and simple silhouettes (+11.2%), ensure room to grow and comfort. Overall, creating a dependable wardrobe of hard-wearing basics is what puts practicality at the heart.

At the more premium supermarket tier, M&S differentiates itself through longevity and function, supported by high-quality natural materials. Cotton, denim (+16.8%), and linen (+24.9%) make up some of M&S’s largest material usage, reinforcing its heritage reputation for quality and comfort. Smaller inclusions of wool (+6.4%), silk (+5.7%), and leather (+14.8%), alongside their fabric innovations of Stay New Technology to prevent fading and pilling, build consumer trust through long-lasting value and craftsmanship, and justify the higher price point.

Next bridges this gap between practicality and premium positioning, again relying heavily on cotton and cotton-elastane blends that prioritise comfort and fit. There is also a growing inclusion of recycled polyester and organic cotton (+28.4%), with recycled fabrics (+17.0%) in general continuing to trend upwards. It suggests that a move towards sustainability would be beneficial in the upcoming market, but is largely missing from competitors at the moment.

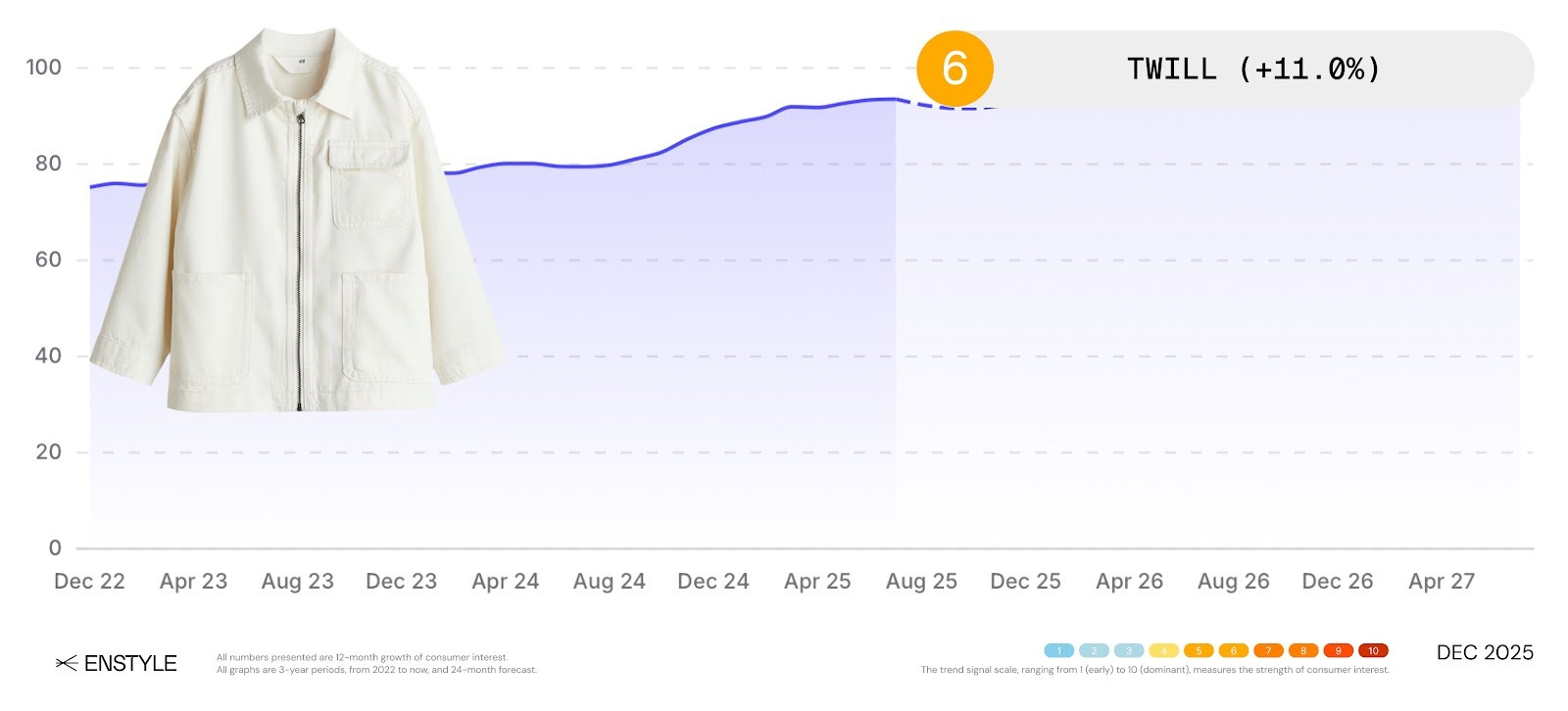

Jack & Jones stands apart through material specialisation, reflecting its roots in denim and utility wear. A higher use of durable fabrics like denim, cotton twill (+11.0%), and leather paired with functional design features such as five-pocket styling and cargo pockets (+11.5%), reinforces its mature, workwear-inspired aesthetic and mini-me alignment with its adult collections.

At the fashion-forward end, Zara relies on synthetics such as 100% polyester (+9.6%) and elastane blends to maintain flexibility and trend agility. The priority is creating widespread appeal by recreating runway styles at accessible prices rather than maximising long-term durability.

Across the market, kidswear collections are shaped by shared priorities of comfort, value, and practicality, especially seen in their material compositions. F&F at Tesco and George at Asda emphasise affordability, with natural fibres and blended fabrics to produce practical, budget-friendly staples, while M&S and Next differentiate through innovative technology and a heavier use of recycled fabrics, which build responsibility and quality. Meanwhile, Jack & Jones and Zara use fabric to enhance their brand positioning and storytelling, one through authenticity and the other through trend responsiveness. These different approaches to fabric usage all share a foundation in function, diversified by different strategies in value and brand identity.

Fashionability and Design

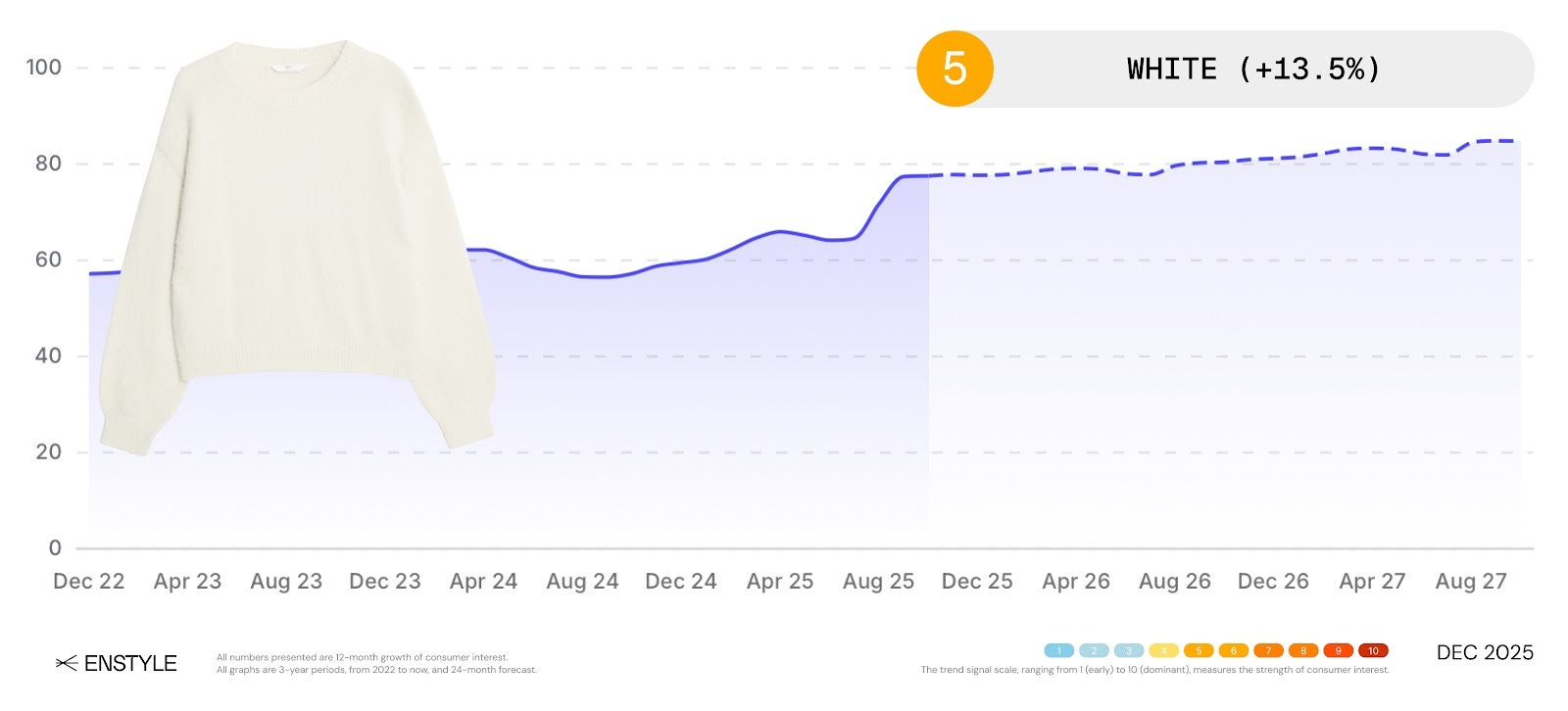

Both F&F at Tesco and George at Asda share similar design philosophies rooted in mass appeal, practicality, and accessibility. The majority of the colour palette heavily features blue (+7.4%), black (11.6%), grey (+11.2%), and white (+13.5%), contrasted with pops of red (+25.1%) and green (+12.7%), for versatility and universal appeal. When looking at design features, F&F focuses on simple, functional features with graphic prints (+7.7%) being the most utilised design element. George adds a more trend-led edge, integrating character graphics (+23.9%) and colour blocking (+137.5%), whilst still maintaining a value-driven price point.

M&S is consistent in a dominant colour base but also introduces a higher amount of yellow (+3.3%). Design details complement the premium feel with the high-quality fabric choices, with embroidery (+9.9%), kangaroo pockets (+3.7%), and patchwork stars. Craftsmanship is evident in the number of pieces that feature full linings and have intricate details like buckles. When paired with neutral and durable fabrics, the collection becomes more elevated and refined in quality, further emphasising M&S’s promise of timeless, reliable designs.

Next continues to maintain its position between practicality and trendiness, featuring signature design elements like graphic prints and embroidered logos. However, the frequent use of patterns such as stripes (+14.5%), plaid (+26.0%), and print (59.4%) positions next firmly within upcoming trends while also appealing to the whole family.

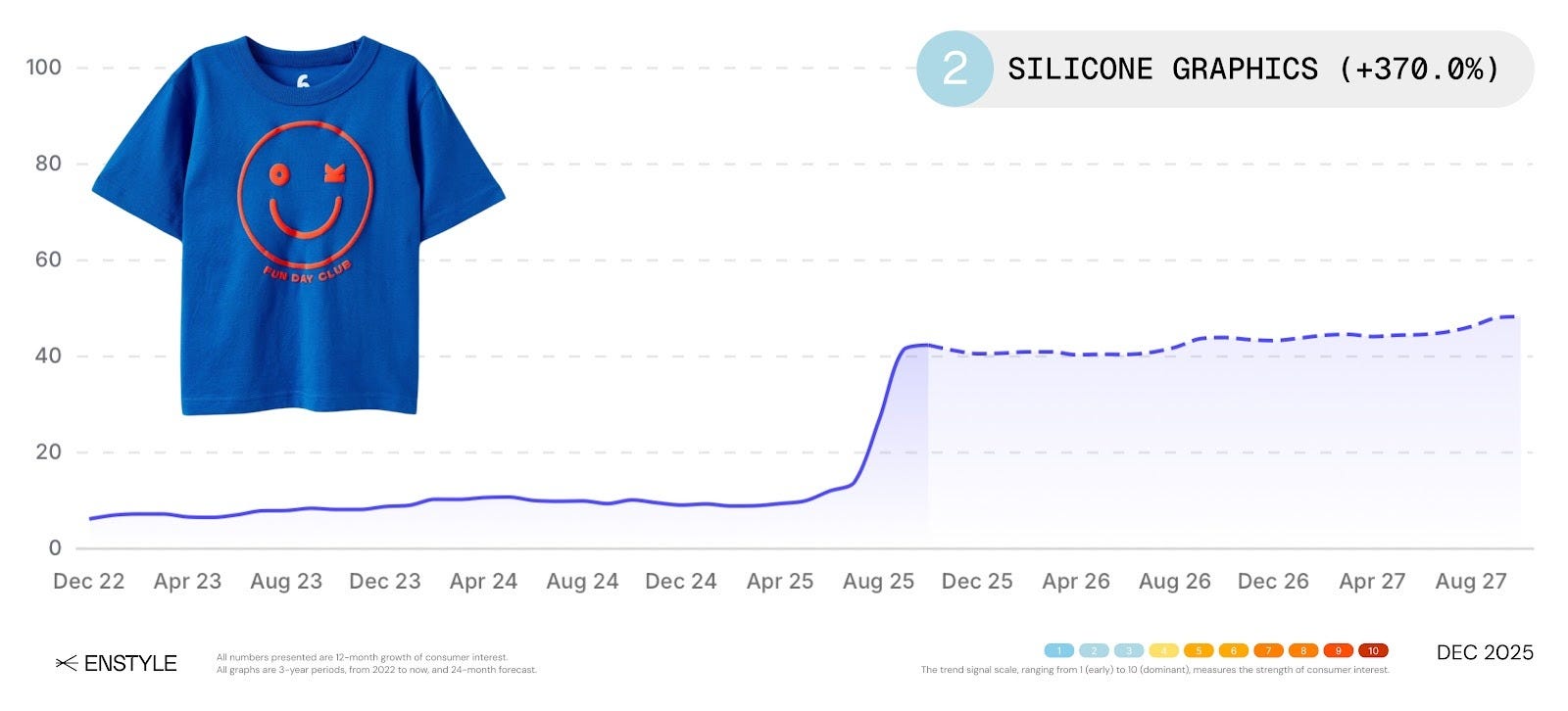

Jack & Jones maintains its utilitarian aesthetic with a more restricted colour palette of black, white, blue, and grey. Design features such as contrast zips, inset sleeves, and functional details like windproof and water-resistant jackets (+5.8%) build on its outdoor-inspired identity. A key element the brand is currently utilising is rubber prints (+370.0%), which successfully aligns trend relevance with brand authenticity.

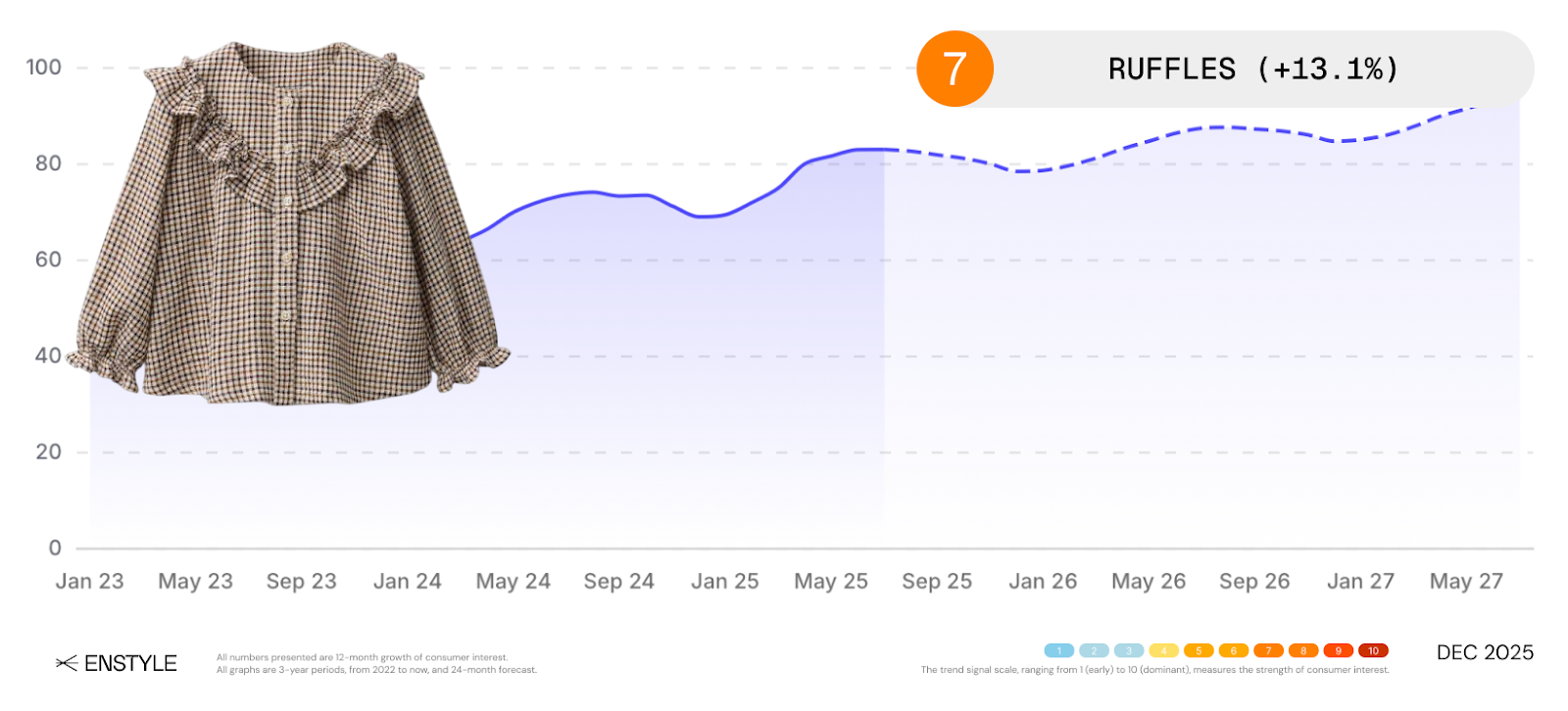

Meanwhile, Zara stands out with its diverse colour palette, with prominent use of green and yellow, which differentiates it from competitors’ core colour choices. Fashion-forward details like graffiti print (+5.2%), ruffles (+13.1%), prints, and label appliqué (+5.8%) translate adult aesthetics into accessible kidswear, allowing for rapid design turnover and continuous freshness.

Across all brands, neutral colour palettes and practical fabrics remain central to consumer appeal, reflecting a growing parental interest in versatile and comfortable clothing (+21.8%). We see parents are increasingly drawn to pieces that fit capsule wardrobes, and can be easily handed down, extending both value and lifespan. Yet, consumer data suggests a parallel desire for more expressive and trendy design elements, from rubber graphics and bold prints to brighter colourways, suggesting an opportunity for brands to combine function with fashion-led detail.

Current Industry Insights

Supermarket brands, F&F Clothing and George at Asda, from the value-centred to premium tiers, are united in their focus on functionality, simple silhouettes and practical fabrics, and an emphasis on ease with easy-to-wash fabrics. M&S represents the more premium end of the supermarket spectrum, elevating simple pieces with higher-quality natural fibres. Next acts as the accessible midpoint by taking the practical foundations whilst also introducing more stylistic range with colour and pattern. In contrast, Zara focuses on the same mass audience through trend-led graphics and rapid product turnover, instead prioritising immediacy. Jack & Jones stands out as the most niche brand, with a strong use of premium materials and a defined aesthetic that appeals to a smaller but highly engaged segment. This creates a market divide based on reaction speed to trends and the balance between function and fashion.

What’s Next for Kidswear

Gender-Neutral Dressing

The kidswear market is moving towards unisex and gender-neutral styles (+14.3%), pushing the sector towards inclusivity and simplicity. This positive trend supports longer garment life cycles, allowing pieces to be worn and handed down across siblings regardless of gender. This trend also builds on the industry’s growing focus on sustainability and supports more cost-effective purchasing.

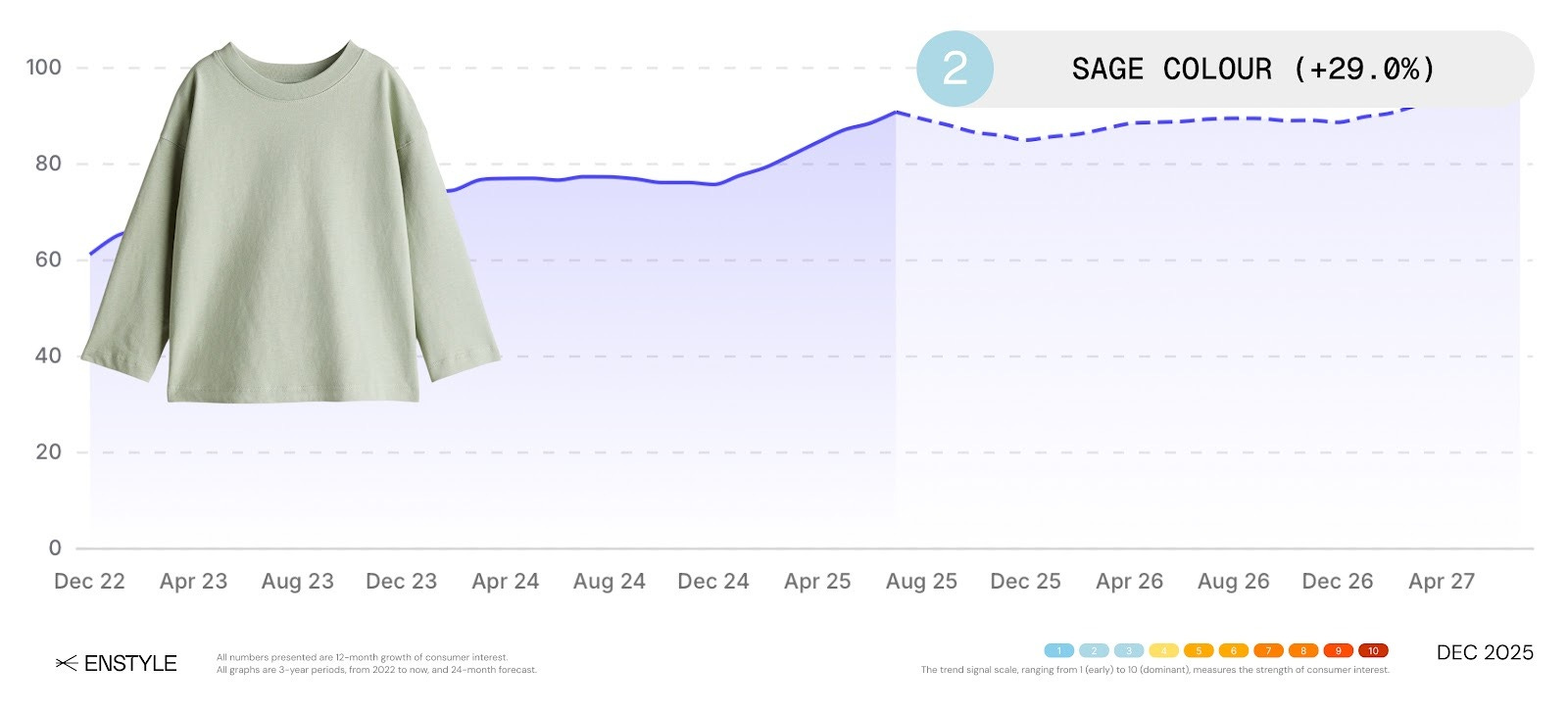

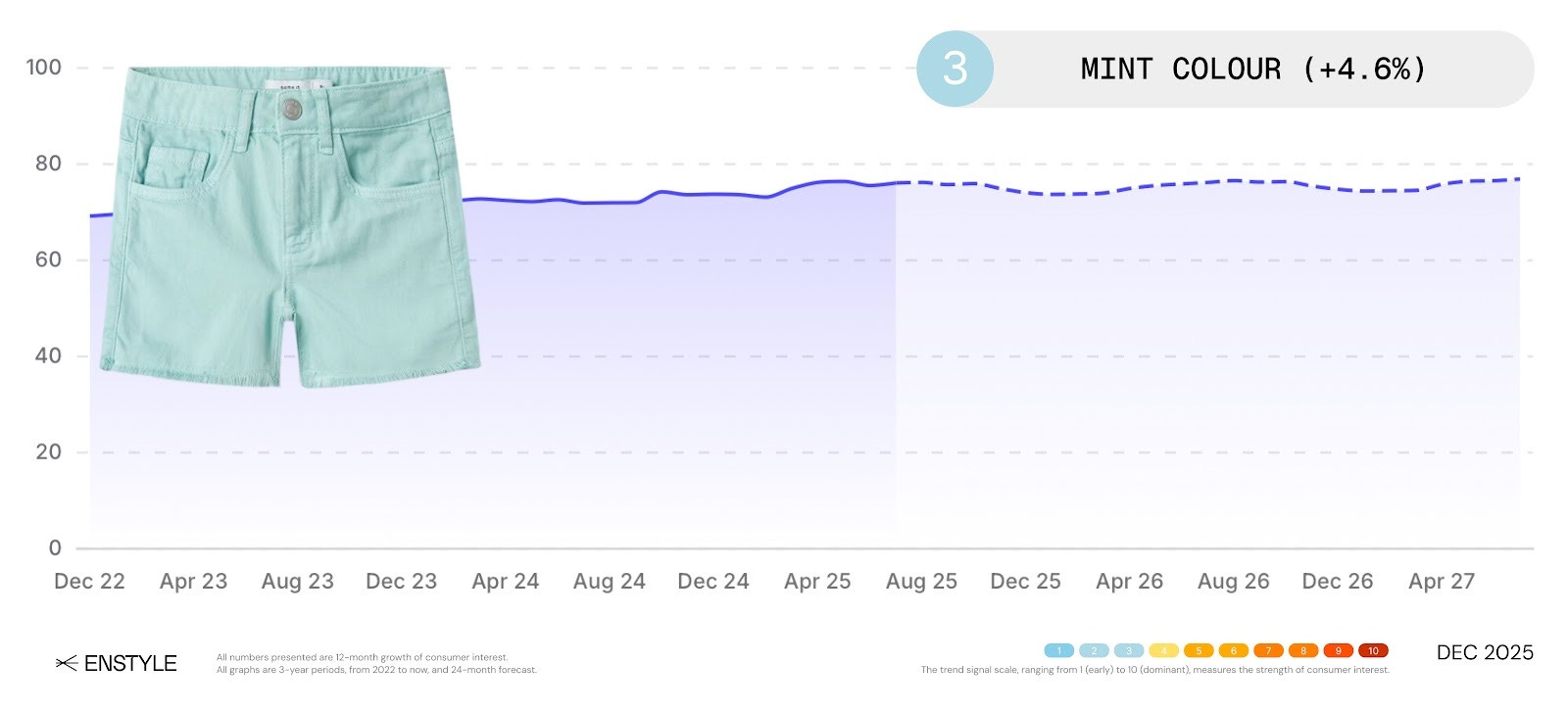

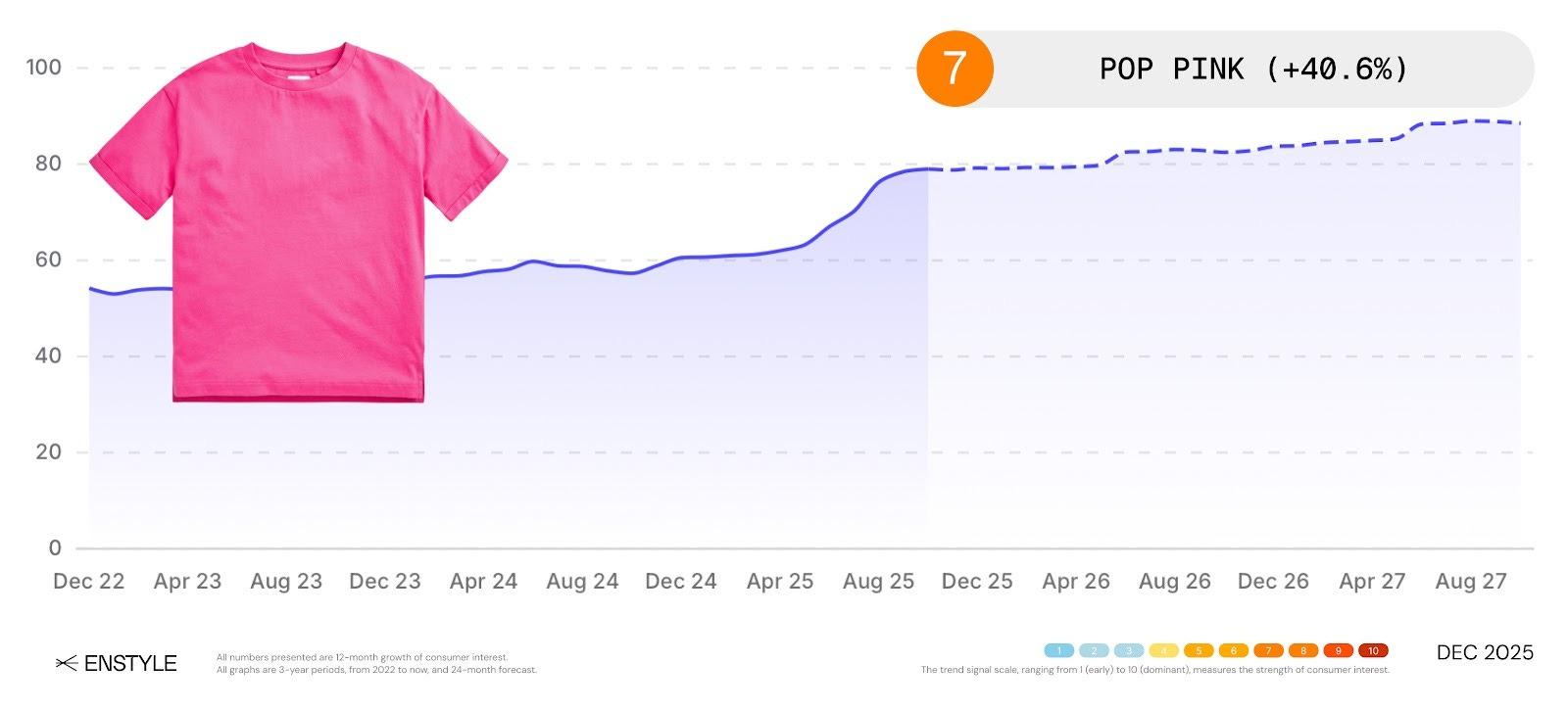

The anticipated increase of colours such as sage (+29.0%), mint (+4.9%), and teal (+11.0%) further reflects a desire for seasonless, gender-inclusive colour palettes. At the same time, bolder tones like fuchsia (+8.6%) could suggest an openness to more stereotypical colours or a continued need for personality and differentiation within minimalistic silhouettes (+20.6%).

Oversized Comfortwear and Athleisure

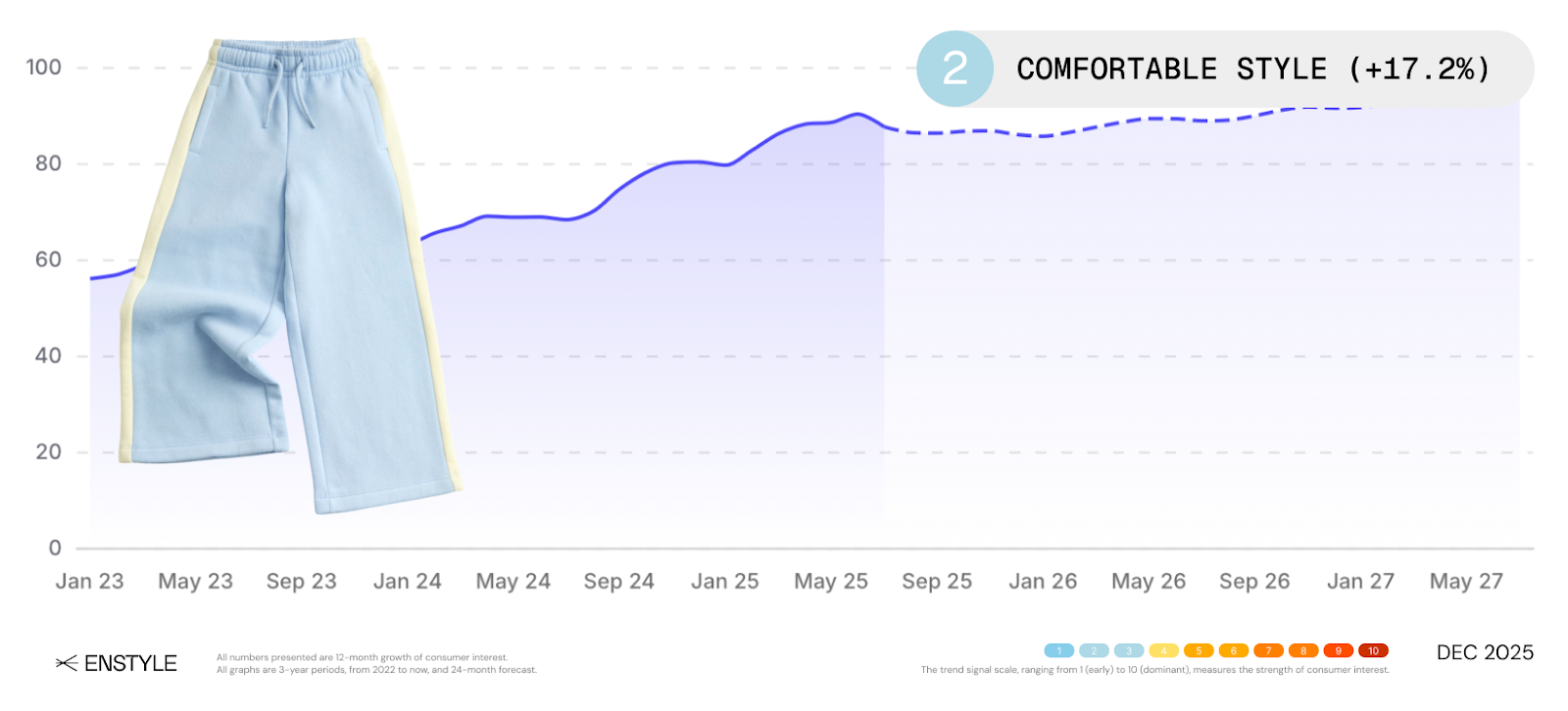

We have already seen how adult trends can influence kids’ clothing, and we are beginning to see this even more with the rise of athleisure (+33.1%) in the kids sector. Just like in men’s and womenswear, we are also seeing the growing popularity of comfort wear (+21.2%) and oversized silhouettes (+45.3%) that cannot only be grown into but also be used as a cosy layer. Similarly to adult fashion, these comfortable styles help to bridge busy lifestyles with mobility. The continued focus on elastic waists, stretchy (+21.5%) and plush fabrics (+1.2%) is the future, allowing brands to cater to both comfort and function.

Easy-Care and Practicality

For the same reasons we see a rise in athleisure, family life is busy and demanding, meaning that convenience is becoming a necessity. Whilst brands have begun incorporating new technology to make garments easier to care for and longer-lasting, demand for these innovations continues to grow, and consumers increasingly expect such advancements at lower price points.

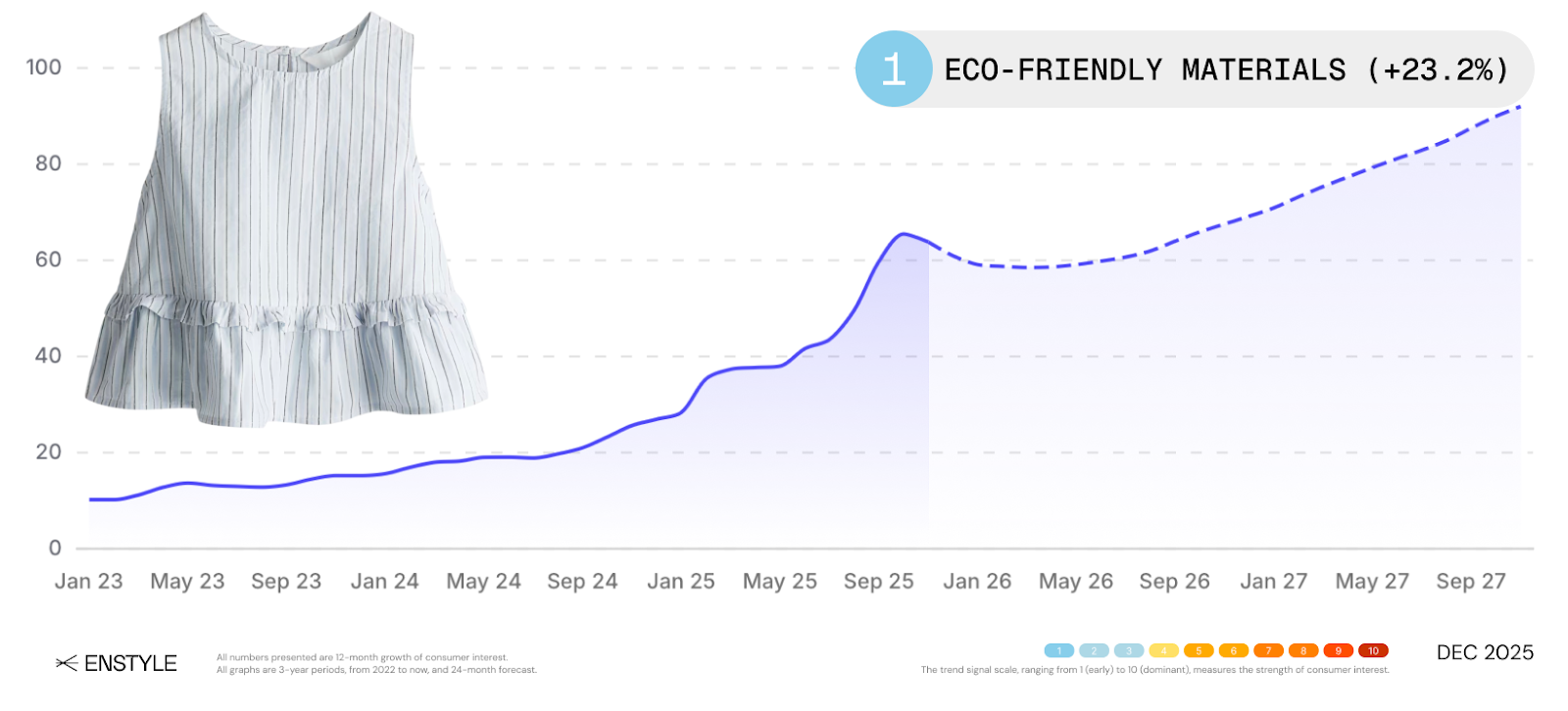

In more premium segments, further investment in natural or recycled materials continues to build trust while aligning with eco values.

Patterns and Designs

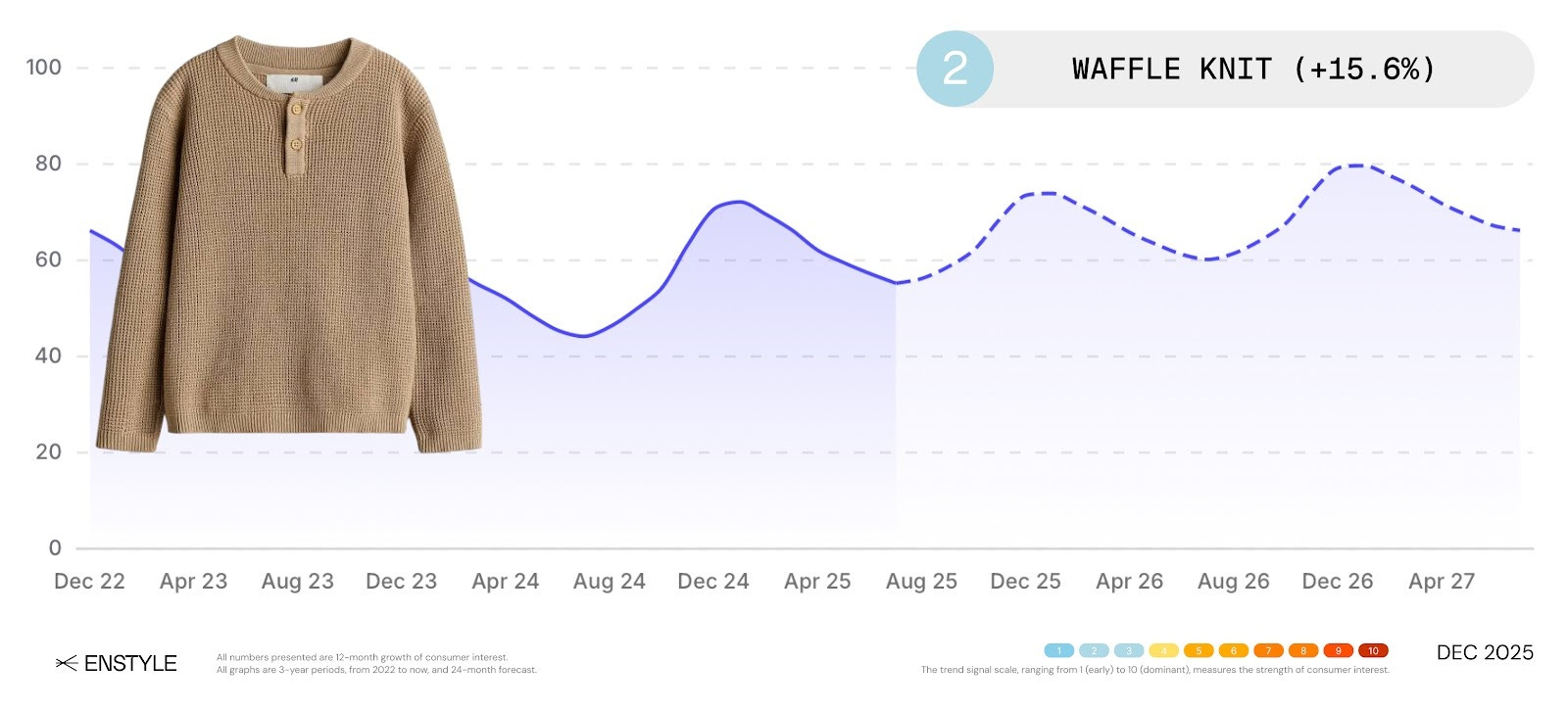

Children’s fashion is also becoming more tactile and playful. The use of crochet (+2.4%), lace (+14.1%), waffle knit (+15.6%), and quilting (+21.2%) introduces greater tactility and texture, helping garments to feel more considered and valuable, whilst also bringing in identity and fun to kids’ fashion.

We also see the rise of small brands like Comfa, which are innovating accessible clothing with discreet fidget toys built into the fabric, helping with regulation and comfort. Whilst this is currently only a niche trend, with the increased desire for accessible clothing, we can expect to see leading brands take similar steps with their collections.

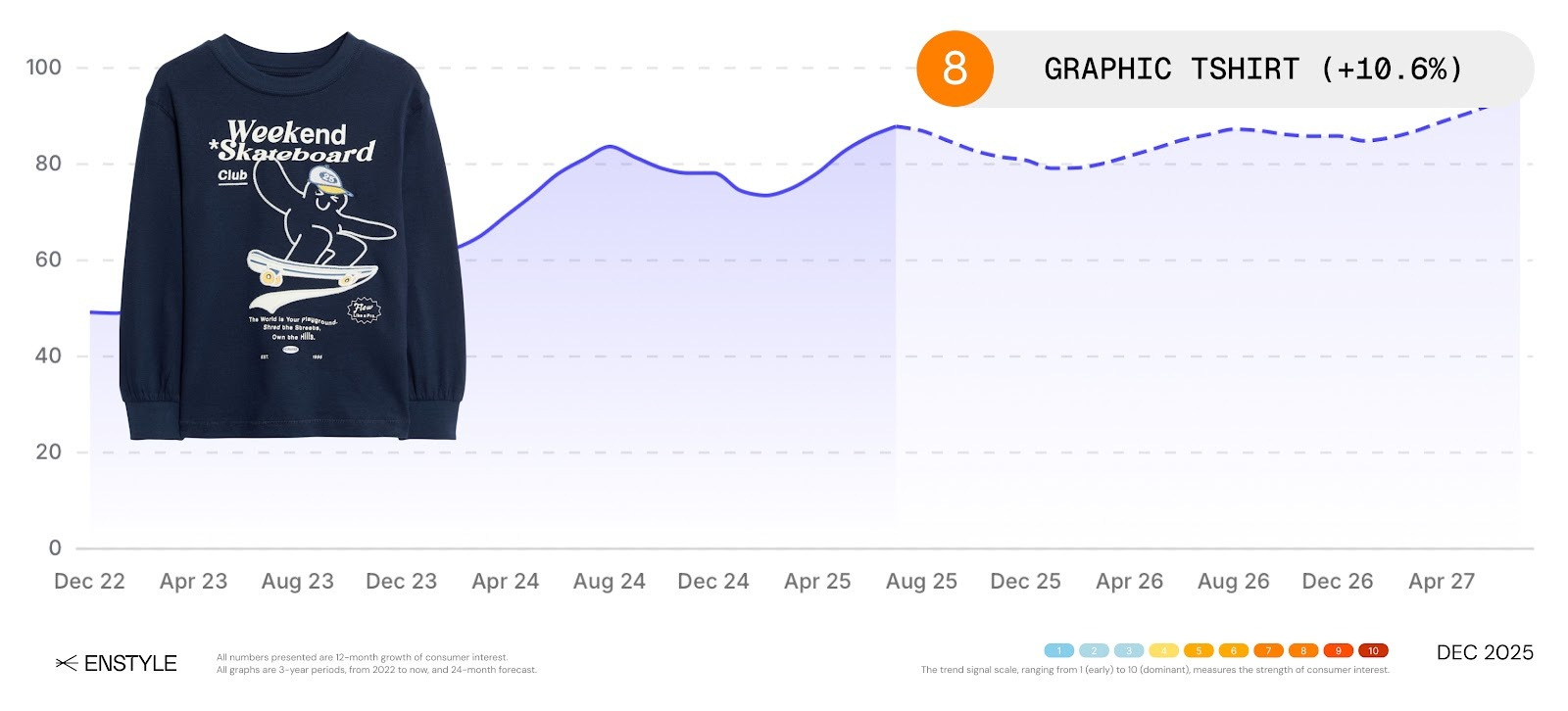

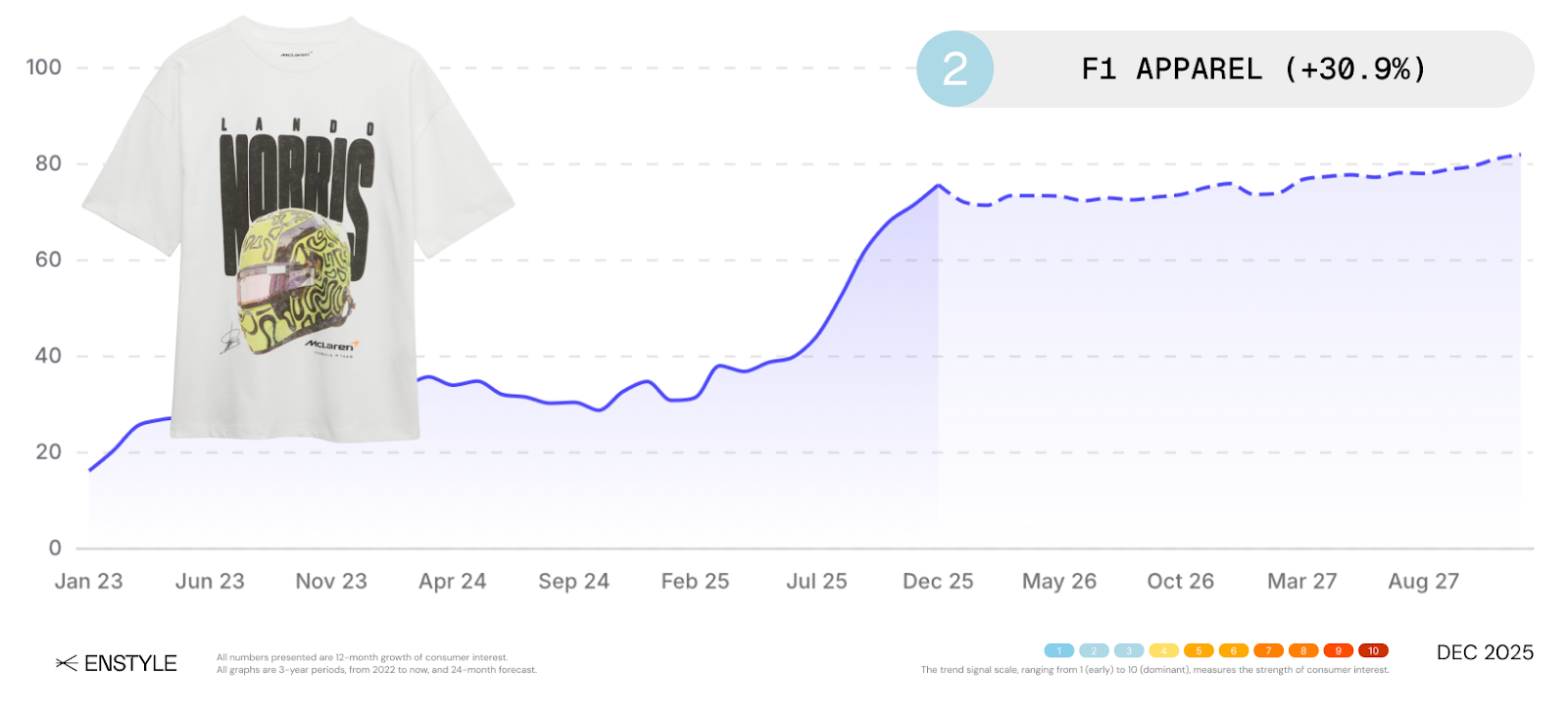

Graphics are also evolving with a sharp growth in pop culture motifs from anime (+274.4%), cars (+45.0%), and sports such as F1 (+35.2%), alongside a resurgence of bold typography (+10.3%). Whilst we have seen a growing interest in minimalistic and androgynous styles, there is also a strong demand for clothing that reflects identity and personality through pieces that speak to children’s niche interests instead of generic graphics.

The Future

The current UK kidswear market is defined by a balance of trend responsiveness and value for money, with key points of differentiation emerging through fabric innovations, from natural and recycled fabrics to polyester blends, that align with parents’ evolving expectations for quality and sustainability. As both style and value continue to grow, we see gender-neutral, oversized silhouettes and seasonless colour palettes are enabling longer wear, extended garment life, and cross-gender usability.

At the same time, as we see kids’ wardrobes become more practical and minimal, there is a parallel rise in bold colours like fuchsia and graphics that reflect children’s unique interests, pushing personality and playfulness back into the category.

The future of kidswear lies in the continued evolution of this balance, with families investing in high-quality, seasonless basics for longevity and trend-driven statement pieces that celebrate individuality and joy.

Stay ahead of fashion shifts

A monthly thread on fashion trends, planning insight, and how AI is shaping design, merchandising, and buying decisions. Written for fashion teams who want clarity, not noise.